Severance payments for employees: Tax peculiarities and optimization possibilities

Introduction

Severance payments are often a welcome financial compensation for employees who leave their jobs. However, without careful tax planning, a large portion of the severance can go to the tax office. In this article, we will show you how to reduce your tax burden using the five-year rule, voluntary pension insurance contributions, and strategic income planning.

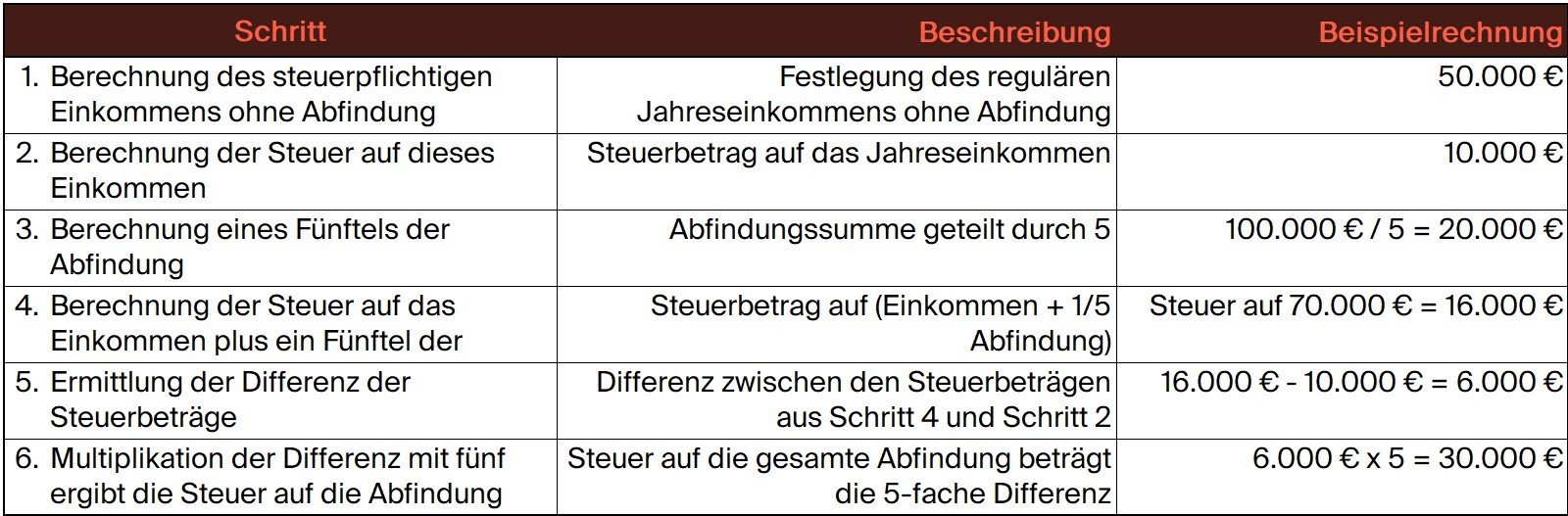

The five-year rule according to § 34 para. 1 EStG is a tax tool to mitigate tax progression on extraordinary income. It allows you to calculate the tax on a severance as if the payment were spread over five years.

How does the five-year rule work?

Data basis: Individual assessment, 2024 simplified without solidarity surcharge.

The five-year rule smooths out tax progression, and you pay less tax on your severance payment.

Voluntary contributions to pension insurance: Double benefits

With voluntary contributions to the statutory pension insurance, you can not only improve your retirement provision but also reduce your tax burden. These contributions are tax-deductible as special expenses, thus reducing your taxable income.

Deferring severance to the following year: Reducing tax progression

Deferring the payment to the following year can make sense if a lower income is expected next year, e.g., due to unemployment, moving abroad, or retirement.

Utilizing tax offsetting - losses from rental or commercial or freelance income

With losses from rental and leasing and from commercial or freelance income, you can further reduce your taxable income. These losses lower the tax burden and can enhance the effect of the five-year rule. This could be achieved, for example, in the following ways:

- High depreciation reduces income.

- Renovation costs can be claimed as deductible expenses.

- Initial losses when starting a business and investment costs reduce income.

Losses should be realistic and recognized for tax purposes.

Important aspects

The tax-optimal structuring of your severance payment requires early and careful planning. By applying the five-year rule, making voluntary contributions to pension insurance, deferring payments, and offsetting losses, you can significantly reduce your tax burden.

Do you want to make the most of your severance payment and save taxes?

Our experts in international tax law are happy to assist you. Contact us today for a non-binding initial consultation and benefit from tailored solutions. Schedule an appointment for a non-binding initial consultation now!