General information on exit taxation for corporations

What is the exit tax?

The exit tax affects individuals who leave Germany and hold significant shares in corporations, among other things. It arises when Germany loses the right to tax the shares held in private assets due to the departure. This mechanism is anchored in § 6 of the Foreign Tax Act (AStG) and typically applies when moving abroad. Although there is no actual sale transaction, a fictional capital gain is taxed. This fictional tax burden consists of income tax, solidarity surcharge, and possibly church tax.

Who is affected?

The exit tax affects you if you have been at least 1% involved in a corporation in the last five years, have given up your residence or habitual abode in Germany, and have been unlimited tax liable in Germany for at least seven of the last twelve years.

How is the exit tax calculated?

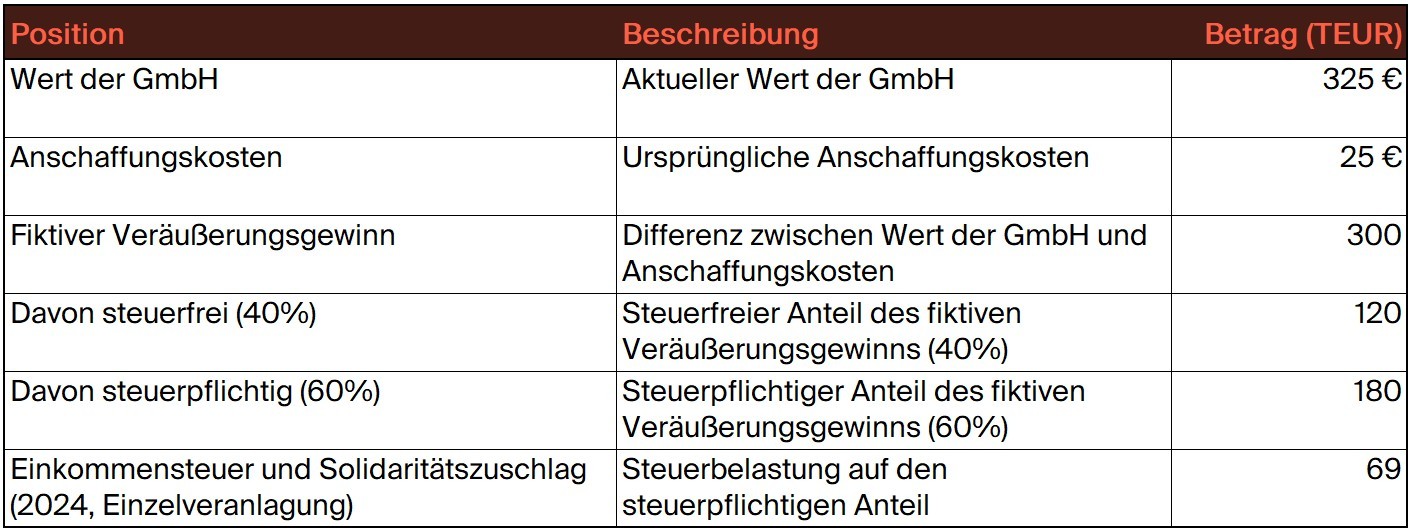

1. The basis is the fair market value of your shares at the time of departure.

2. The original acquisition costs are deducted from this value.

3. 60% of this fictional capital gain is subject to your personal income tax rate, but at most 45%, plus solidarity surcharge and possibly church tax. The partial income procedure relieves you in this case, so that 40% of the gain remains tax-free.

Example

Are you affected by the exit tax? We can help you!

We provide individual advice to minimize your tax burden and avoid unexpected costs. Whether avoidance, reduction or international tax issues - our expertise is at your service.

Act now! Contact us today to learn more and develop a strategy tailored to your needs. We look forward to hearing from you! Book your initial consultation!